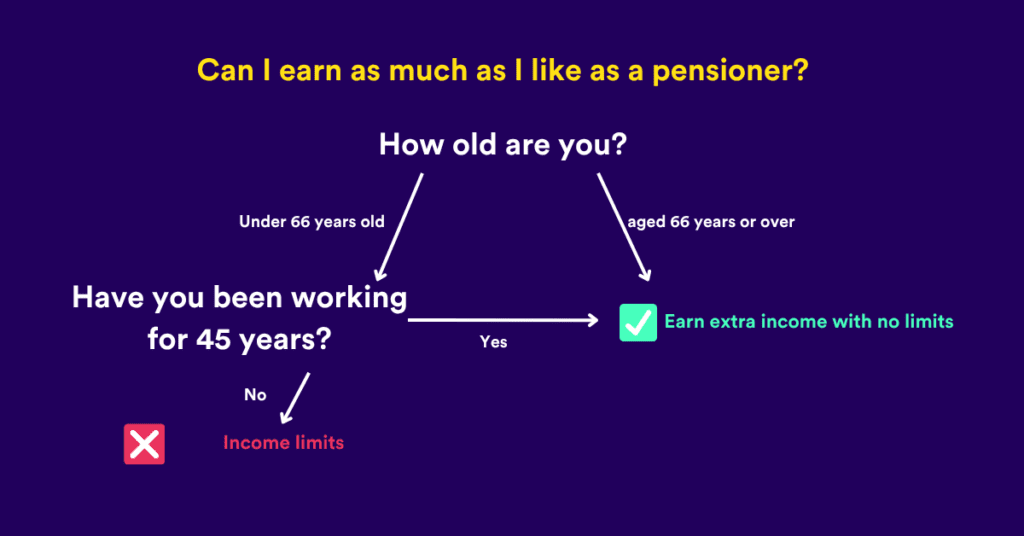

As a self-employed pensioner in Belgium, you are allowed to earn additional income under certain conditions. The amount of additional income permitted depends on your age, length of service and the type of pension you have received. Below is a summary of the rules applicable in 2026.

Do you also have a flexi-job? If so, since January 2025 there has also been an income limit for flexi-jobs. Self-employed income and flexi-jobs have separate as well as combined rules. This can make things complicated, but we explain everything with examples. That way, you can sleep soundly.

✅ Unlimited additional income

You may earn unlimited additional income without affecting your pension if:

- You have reached the statutory retirement age (66 years in 2026).

- You retired before the statutory retirement age, but can demonstrate a career of at least 45 years at the time of retirement.

In these cases, you may continue to work as a self-employed person without any income restrictions.

⚠️ Limited additional income

If you have not yet reached the statutory retirement age and cannot demonstrate a 45-year career, or if you have only received a survivor’s pension, income limits apply. For self-employed activities in 2026, the net annual income limits are as follows:

Statutory retirement pension income limits

- Without dependent children: €8,346

- With 1 dependent child: €12,519; for each additional dependent child, the amount is increased by €4,711

Survivor’s pension income limits

- Without dependent children: €18,844

- €28,266 with 1 dependent child; for each additional dependent child, the amount is increased by €4,711

If you exceed these limits, your pension will be reduced in proportion to the amount by which the limit is exceeded. If you exceed the limit by 25% or more, you will experience a loss of a quarter of your statutory pension. If you exceed the limit by 100% or more, your pension will be suspended for the entire calendar year.

👩💼 Flexi-jobs and other additional income

For pensioners in flexi-jobs, an additional income limit will apply from 1 January 2025. If you have not yet reached the statutory retirement age and your career spans less than 45 years, you may earn a maximum of €7,876 per year in a flexi-job.

⚠️ But be careful: the general income limit discussed above also remains in force. This means that your net taxable income as a self-employed person and your income as a flexi-jobber are added together for the purposes of the general limit.

If your flexi-job income exceeds this limit, your pension will be reduced proportionally by half the percentage of the excess.

This is therefore less than for a self-employed person, where the pension is reduced entirely proportionally by the percentage of the excess.

So be careful if you combine flexi-jobs with self-employment

If you combine a flexi-job with self-employment, both income limits are taken into account.

The general income limit and the flexi-job limit. Your pension could therefore be reduced twice if you are not careful.

📌 Important points to note

- The statutory retirement age is rising gradually: 66 years from 2025, 67 years from 2030.

- Additional earnings must be correctly declared to the Federal Pension Service.

- Exceeding the permitted limits may also have consequences for social security contributions.

🤔 This table summarises the income limits for pensioners

| Situation | Is unlimited additional income permitted? | Permitted net annual income (self-employed activity) |

| You have reached the statutory retirement age (66 years in 2026) | ✅ Yes | No limit |

| You have not yet reached the statutory retirement age, but have a career of at least 45 years | ✅ Yes | No limit |

| You have not yet reached the statutory retirement age and have a career of less than 45 years | ❌ No | €8,093 with no dependants €12,140 with 1 dependent child +€4,711 per additional child |

| You receive only a survivor’s pension, regardless of your age or length of service | ❌ No | €18,844 without dependants €28,266 with 1 dependent child +€4,711 per additional child |

| You combine a retirement pension with a survivor’s pension and have reached the statutory retirement age | ✅ Yes | No limit |

| You combine a retirement pension with a survivor’s pension, but have not yet reached the statutory retirement age and have less than 45 years of service | ❌ No | €18,844 without dependants €28,266 with 1 dependent child +€4,711 per additional child |

| You are in a flexi-job and have not yet reached the statutory retirement age and have less than 45 years of service | ❌ No | €7,876 (regardless of number of dependent children) |

⚠️ What if you earn more than the income limits?

It is very important to take these income limits into account. If you exceed them, you could easily experience a loss of pension compared to the extra income you have earned. You would then have worked hard, only to end up with less.

The general income limit

Example 1: Ann is self-employed and must take the income limits into account

Ann is 64 years old and retired. She has not yet reached the statutory retirement age and does not yet have a 45-year career. She must therefore take the income limits into account.

She has a net taxable annual income of €10,000 from her self-employed activities. This is more than her income limit of €8,093 – exactly 24% more.

Her retirement pension of €25,000 is therefore reduced by 24% and now amounts to €19,201. Together with her income from self-employment, she is left with €29,201.

Example 2: Els is self-employed and must take the income thresholds into account

Els must also take the income thresholds into account. She earns considerably more than Ann and has ultimately earned €17,000 from her self-employed activity. This is more than 100% above the threshold of €8,093. As a result, her pension is completely cancelled.

As a result, she is left with only her €17,000 from her self-employed activity.

Please note!

Els earned €17,000, but ultimately ends up with less than Ann due to the income limits.

The flexi-job income limit

Would you like to do a flexi-job too? You can! But if you haven’t yet reached the statutory retirement age and don’t have a career of 45 years, you’ll need to take two income limits into account.

Example 3: Julie is 63 years old, self-employed and a flexi-jobber

Julie is a real go-getter and, during her retirement, is involved in both a flexi-job and self-employment activities.

She earns:

- As a self-employed person: €2,000

- As a flexi-jobber: €10,000

The first general limit has therefore been exceeded. She earns €12,000, which is 48% more than permitted. Her pension of €25,000 is therefore reduced by €12,069, leaving her with €12,931.

But then there is the flexi-job limit. She has also exceeded this limit by 27%, so her remaining pension is reduced once again by half of the 27%, i.e. 13.5%.

She is ultimately left with just €11,185 in pension. Together with her additional earnings, she has a total of €23,185

😳 This is less than what she would have been left with if she hadn’t worked. Not very smart of Julie, then!

🎉 Earning extra pays off, as long as you stick to the income limits!

But: don’t panic! As long as you stay within the income limits, there’s no problem. For example, if you earn €7,000 (which is less than the income limit of €8,093), you can add this to your pension without any issues.

So if you have the same pension as Ann, Els and Julie, you’ll be left with a whopping €32,000 instead of your €25,000 pension. A nice bonus!

🔍 More information

For a detailed summary and personalised simulations, please visit the website of the Federal Pension Service.

If you are considering earning extra income as a self-employed person after retirement, it is advisable to seek professional advice to avoid any unpleasant surprises.